Below we are publishing the second part of the opening report given by Nick Beams to an international school held by the International Committee of the Fourth International (ICFI) and the International Students for Social Equality (ISSE) in Sydney, Australia from January 21 to January 25. Beams is a member of the international editorial board of the World Socialist Web Site and the national secretary of the Socialist Equality Party of Australia.

The first part was posted January 31. Part three will be posted on February 2.

The financial crisis in the US and the expanded growth of the world economy, especially over the past seven years in the less developed countries, are not separate events, but different sides or aspects of a single process.

To put it in a nutshell: The expanded growth of China (along with other countries) would not have been possible without the massive growth of debt in the US. But this growth of debt, which has sustained the US economy as well as global demand, has now resulted in a crisis.

At the same time, low-cost production in China and other regions, and the integration of these regions into the world economy, lowered inflationary pressures. This process created the conditions for lower interest rates, thereby fueling the expansion of credit which has played such a vital role in sustaining the US economy and the world economy as a whole.

Let us examine this process in more detail. The latest financial crisis has not come out of the blue. It has been created by the response to previous crises going back to the stock market collapse of 1987. At that time, incoming Fed Chairman Alan Greenspan opened the credit lines to ensure the stability of the market.

The first years of the 1990s, following the recession of 1991-92, were characterised by slow growth—the so-called “jobless recovery.” But by the middle of the decade there was a shift. In 1996, Greenspan pointed to an upsurge in stock prices which was playing a key role in lifting the US economy and, in a speech at the end of the year, warned of “irrational exuberance.”

But after a brief attempt to increase interest rates, which met with a hostile reaction from Wall Street, Greenspan moved to cut rates. When the Asian crisis broke in 1997, US President Bill Clinton referred to it as a “glitch,” while Greenspan insisted it was a result of Asian “crony capitalism” and the failure to adopt the methods of the “free market.” Indeed, it was said to be a further confirmation, following the collapse of the Soviet Union and the other Stalinist regimes, of the historical superiority of the Anglo-Saxon “free market” system.

Within months, however, it became clear that the crisis in Asia was a symptom of deeper problems. In August 1998, Russia defaulted on its international debts and in September the hedge fund Long Term Capital Management had to be bailed out with a $3 billion rescue operation lest its collapse set off a systemic financial crisis. The response of the US Federal Reserve was to cut interest rates.

As a result, the economic storms appeared to pass relatively quickly and the US economy underwent a boom at the end of the decade, hailed as the dawning of the era of the “new economy.” In fact, as the stock market reached record highs, the rate of profit had begun to turn downward and the increased profits turned in by companies such as Enron and WorldCom were revealed to be fictitious. The stock market bubble collapsed in 2000 and the US economy experienced a recession, leading to the loss of three million manufacturing jobs.

The downturn, however, was relatively short-lived, and the US economy entered an upturn, but one characterised by a number of peculiar features. While it was based largely on increased consumption spending, this was not the result of higher wages and employment growth—real wages remained virtually stationary—but an increase in consumer debt, made possible by the cutting of interest rates by the Federal Reserve Board. These cuts fueled a housing boom, which in turn made possible the increase in consumption spending.

One of the key factors which made possible the low interest rate regime so central to economic growth was the investment by Chinese authorities of vast amounts of finance capital in US assets.

This recycling of Chinese trade surpluses back into the US financial system seemed to complete a virtuous circle. The inflow of capital through purchases of US Treasury notes and other forms of debt enabled the Fed to keep down interest rates, which in turn helped fuel the housing market, which in turn financed increased consumption spending, providing a market for the expanded output from China and increasing the Chinese trade surplus with the US, which was then invested in US financial markets. This process was at the heart of the growth in the world economy after the US recession of 2000-2001.

The injection of large amounts of credit into the financial system has played a key role in sustaining the US and world economy. But credit does not simply disappear once its work in reviving the economy is done. Rather, it contributes to a buildup of finance capital within the global economy, with major implications for the stability of the system as a whole.

Looking back over the past quarter century, we find, according to Greenspan, that as a result of lower nominal and real interest rates, asset prices worldwide have risen faster than nominal gross domestic product (GDP) in every year since 1981, with the exception of 1987 and 2001-2.

What are the implications of this process? The first point to note is that stocks, real estate and other forms of property titles, financed by credit, are all, in one form or another, claims to income. That is, in the final analysis, they are claims to the surplus value which is extracted from the working class.

The value of such assets can rise faster than GDP provided that the proportion of national income going to profits is increasing—that is, if there is a greater pool of surplus value to draw from. But the process in which asset values, claims on income, rise faster than GDP cannot continue indefinitely.

An indication of how far the process has gone was provided in an article in the Financial Times of June 25, 2007. It noted that prior to 1995, the ratio of personal sector wealth to GDP in the US tended to fluctuate at about an average of 3.4 to 1. The article noted: “Now, despite the paucity of savings in the US economy, the ratio stands at 4.1 to 1. A return to the long-run average would imply a fall in US personal net worth of approximately $10,000 billion. With similar trends mirrored across much of the world, total global losses from the coming financial meltdown could easily reach $25,000 billion to $30,000 billion.”

According to the McKinsey Global Institute, by 2005 the stock of global financial assets had reached $140 trillion—that is, more than three times global GDP. This compares with the situation in 1980 when the stock of global financial assets and global GDP were roughly equal.

If we come to the US mortgage market, it is clear that for much of this decade it has taken the form of a Ponzi scheme. That is, assets in the form of mortgage debts derived their value not from the expected stream of income payments—it was clear that in the case of subprime loans there was no possibility of keeping up payments—but from the expectation that the value of the underlying asset would keep rising as more credit became available and boosted the market. And a rising market meant that greater risks could be taken because the assets backing the debt—houses—had risen in value.

In 2001, subprimes accounted for 8.6 percent ($190 billion) of mortgage originations. By 2005, this had risen to 20 percent ($625 billion). These mortgages were then sold off in the form of financial assets. In 2001, so-called securitised subprimes amounted to just $95 billion; by 2005 this had grown to $507 billion.

In previous times banks that originated mortgages had to assess the risk. This was the era of so-called 3-6-3 banking: Borrow money at 3 percent, lend it to home buyers at 6 percent, and head for the golf course at 3 o’clock.

In the new financial world risk assessment was to a great extent done away with. There was no need for mortgage originators to undertake this task because the mortgage would be sold off to another institution. The mortgage originator would not bear the risk. How was risk supposed to be assessed? By the risk assessment agencies such as Standard and Poor’s, Moody’s and Fitch. They played a vital role in ensuring that the debt packages based on subprime and other risky mortgages were given a high rating. And it was in their interest to do so.

According to one recent study of the subprime crisis, fees paid to the rating agencies for helping to market mortgage bonds “were about twice as high as they were for rating corporate bonds—the traditional business of ratings firms. Moody’s got 44 percent of its revenue in 2006 from rating ‘structured finance’ (student loans, credit card debt and mortgages)” (L Randall Wray, “Lessons from the Subprime Meltdown,” Levy Economics Institute, December 2007, p. 21).

Now the whole subprime market has collapsed. It is estimated that “well over a trillion dollars of subprime US mortgages will lose one half their value” (Wray, p. 22).

The expansion of credit not only boosted house prices, but led to an even bigger increase in debt. “[W]hile real estate values easily doubled over the past decade, from $10 trillion in 1997 to well over $20 trillion by 2005, home mortgage liabilities rose even faster, from less than $2 trillion in 1997 to $10 trillion in 2005. (Indeed, between 2002-06, total credit grew by $8 trillion while GDP only grew by $2.8 trillion)” (Wray, p. 27).

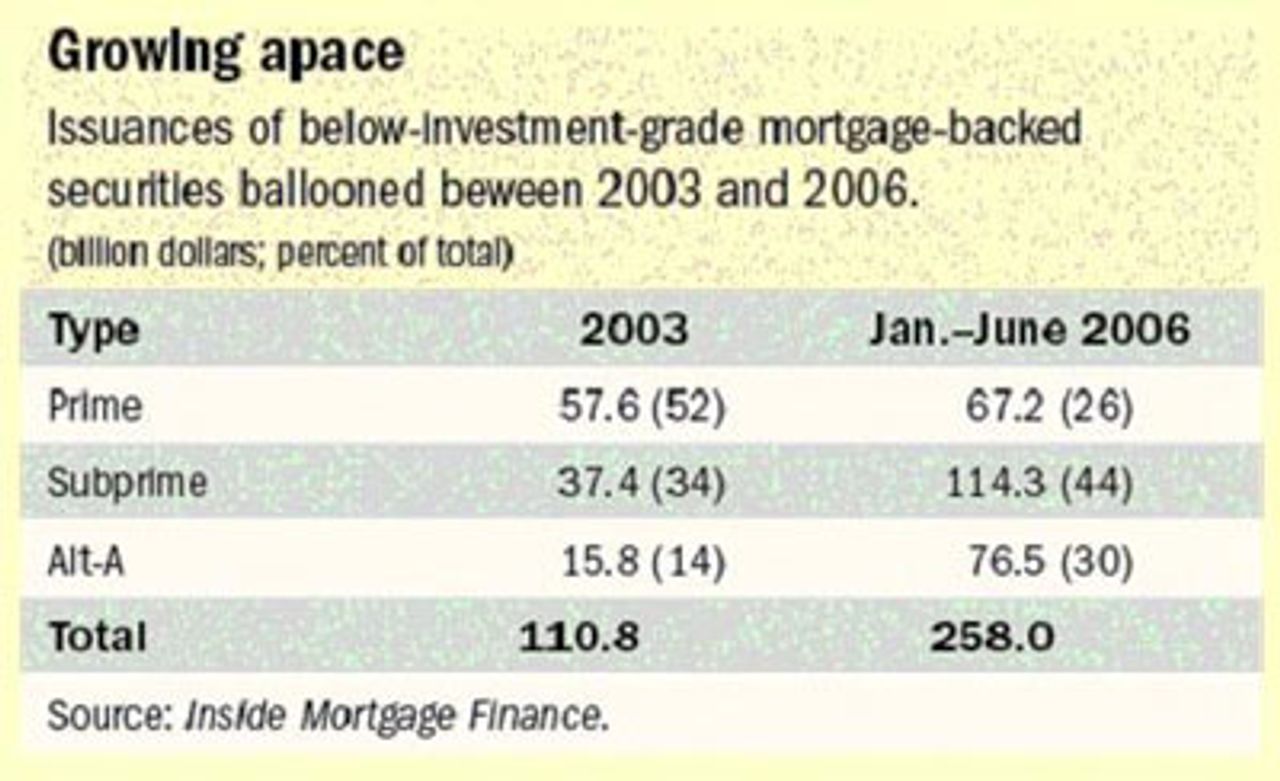

One of the chief mechanisms for the creation of this financial bubble has been the securitisation of mortgages—the aggregation of large numbers of mortgages into debt packages which are then sold off. This was supposed to shift risk off the balance sheets of banks and other financial institutions. But what has happened is the risk that was sent out the front door has come in the back because the risky debts have been purchased by off-balance sheet organisations set up by the banks—so-called “structured investment vehicles” (SIVs). The increased role of subprime mortgages in the creation of these securities is made clear in the following table published by the IMF.

The securitisation process has meant that, via a roundabout route, banks now hold packages of mortgages originated by organisations that had no interest in evaluating whether they could be serviced. This means that banks now hold the debt of borrowers whose risk has never been assessed. This process, which returned large profits, was based on one crucial assumption: that the continuous supply of credit would ensure that house prices would keep rising, so there was no need to assess the risk of the borrower because in the case of default the house could simply be sold off and realise more than the purchase price.

That assumption held good for about a decade after 1994 and only began to turn sour in 2005-2006 when they began to decline. In 2004 the Case-Shiller home-price index increased 20 percent over the previous year. In 2006 it declined 5 percent.

There was a fundamental flaw in the housing bubble—the income of the vast majority of working class families, which must be used to pay off mortgage debt, has been decreasing or stagnant since the end of the last recession in 2001. In the past eight years, the level of US GDP has increased by more than a quarter, while median wages have fallen by 4 percent.

The financial problems go beyond the subprime mortgage market. In the commercial paper market—where firms raise cash through the issuing of short-term debt—there is about $2.2 trillion outstanding, of which $1.2 trillion is backed by residential mortgages, credit card receivables, car loans, and other bonds. There could be as much as half a trillion dollars of potentially worthless paper held by the biggest banks (Wray, p. 36).

Now there are warnings (see e.g., Financial Times, January 14, 2008) that credit default swaps, an insurance system for debts, could be the next area to experience a crisis.

No one really knows the full extent of the losses. When the subprime crisis was starting to break, Bernanke estimated the losses in the range of $50 billion to $100 billion. Now, expected losses range from $300 to $400 billion. But it could be much more. According to one estimate, if house prices fell by as much as 30 percent, credit losses could reach $900 billion. (See Jan Kregel Minsky’s “Cushions of Safety,” published by the Levy Institute).

Apart from the situation facing the banks, there is the issue of the impact of the housing slump on the level of consumption spending in the US, which plays such a decisive role in providing a market for the goods manufactured in China and the rest of Asia.

With real incomes stagnant or falling for all but the top 20 percent or so of the American population, the increase in house prices has played a crucial role in financing the increasing debt incurred by large sections of the population. Since 2002, home equity cash-outs have totaled $1.2 trillion, equivalent to 46 percent of the increase in consumption spending over this period. The social consequences are enormous, as David North made clear in his report to the national aggregate of the SEP in the US held earlier this month (See “Notes on the political and economic crisis of the world capitalist system and the perspective and tasks of the Socialist Equality Party”).

“Thus, the collapse of housing prices deprives the broad mass of working Americans of one of the principal means by which they have sought to counteract the financial burdens created by three-and-a-half decades of wage stagnation. The income of a male worker in his 30s is now 12 percent below that of a worker the same age in 1978. As former Labor Secretary Robert Reich has noted, the ‘coping mechanisms’ that have been employed to deal with wage deflation have been the massive movement of women into the work force (from 38 percent in 1970 to 70 percent today), and the addition of two weeks to the annual work load. Americans work 350 hours longer per year than the average European.

“By the turn of the 21st century, when workers reached the physical limit of their ability to make money by working, they began to depend more and more on borrowing, using their homes as collateral. As this means of bridging the ever-wider chasm between income and needs disappears, millions are faced with the specter of falling into the financial abyss. Already, during the first half of 2007, personal bankruptcies in the United States increased by 48 percent. The extent to which workers are stretched financially to the limit is exposed by the fact that 27 million workers will have to borrow money this winter simply to pay their heating bills. But the use of credit cards is becoming just as problematic as home equity loans. As all the traditional and individualistic means for coping with prevailing economic realities recede, the working class is forced to turn to the only means by which it can defend itself—that of collective and conscious social and political struggle against the capitalist system.”

In his analysis of the role of debt in sustaining this process, L Randall Wray of the Levy Institute makes the point that a financial crash is not necessary to turn a slowdown into a deep recession.

“All else equal, if the private sector were to reduce spending to, say, only 97 cents per dollar of income, this would lower GDP by half a dozen percentage points. And if the private sector were really spooked, it might reduce spending to 90 cents on the dollar—as it usually does in a recession—taking a trillion-and-a-half dollars out of GDP, leaving a huge gap that is unlikely to be fully restored by exploding budget deficits or by exports” (Wray, p. 44).

It is clear, even from this limited range of statistics, that the world capitalist order is facing a series of problems which have struck at the very heart of the global financial system. Martin Wolf of the Financial Times warns that it is the end of the Anglo-Saxon model; Malcolm Knight, the general manager of the Bank for International Settlements, points to the collapse of the “originate and distribute” model which has been at the centre of financial innovation over the past decade.

There is widespread acknowledgement that the financial methods and practices developed over the past period have created serious problems. However, these methods were not devised by some rogue traders who happened to take control. They were endorsed at the highest levels of banking and finance and were bound up with developments in the global economy itself. It is not a matter, therefore, of simply trying something else, or reverting to less risky methods, as if it were a question of trying on another pair of shoes.

There is now wide recognition that the credit crunch has major implications for the stability of the world capitalist economy.

To be continued